20

January

2023

If history has taught us one thing, it is that extraordinary facts can result in great changes. Despite being unknown and unpredictable the world economy was significantly shaped by the great depression, the 9/11 events, and the pandemic. For instance, the 9/11 attacks prompted the FED to reduce interest rates, which inflated the housing bubble and sparked the 2008 financial crisis. Numerous interactions have been brought on by the pandemic. The jump of the container freight rate index, the reappearance of the inflation monster, and the subsequent inflation inflating of interest rates on a global scale… How these interactions are going on.

It is obviously impossible to quantify the freight index's influence on global trade, even if we accept that it is a significant factor! If we need to make a quick impact assessment it can be said that the most severe effects are concentrated on the profit-loss balance of trade and routes, There is no doubt that the freight rate is a value which has an impact on the volume, loss and profit of trade. Those of our readers who are interested in business valuations are aware that businesses' value rises when the freight rate index rises and also suffer losses when the freight rate index falls. Because it directly affects costs.

In addition to its impact on profit and loss, it can change trade routes or be affected by these changes. Let's start with an example. Due to China's "zero cases" policy, some businesses have shifted their production to low-cost nations with fewer restrictions. But it's crucial to remember, that only some companies have been successful in doing this. Because producers and investors cannot be immediately persuaded to move despite China's abrupt and radical decisions scaring them away. First of all, we need to take a look at the infrastructure of alternative countries. Are the factories, infrastructure, ports, etc. sufficient to provide production?

Let's come to the freight rate dimension of the issue! China imposes low freight rate tariffs on its exports. Are there any other countries that could offer the same benefit? Very difficult! If we think for a moment that this freight rate advantage is also provided by others; The problem arises that only 5 percent of the products exported from China are exported from other countries. What kind of an outcome does it create in terms of both the freight rate and the infrastructure? Since some imports are required for exports, the effect of this 5 percent foreign trade change will be approximately 12 million TEU/year. We can estimate that it is as much as the TEU volume of an average economy-annually. In conclusion, trade that leaves China may revitalize the nation where it goes, but we must not forget the port investments that must be made to serve this additional volume.

So in what direction will the freight index go?

Assuming that what we mentioned above will not be realized, that is, Chinese exports will not be directed to other countries, it seems that it would be a mistake to expect an upward movement in the freight rate index.

When we regard the freight rate index, it should not be forgotten that container ship orders have started to be postponed. Reduced density at major ports, end of waiting times, and return to a more reliable service network... These advancements allow freight rate index to continue to fall or move in a saw motion at these levels (moving up and down). If the freight index keeps declining, it will fall for two consecutive years, setting an example in the future. The only exception to this rule is the distinction between those who have annual freight rate contracts and those who conduct spot business, but that in itself may be the subject of a separate article.

Under normal circumstances, the scenarios based on the freight rate index are the interpretation of the above events and all other estimates by throwing them into a mixer. Of course, the freight scenarios written at the beginning of 2022 did not take these developments into account, but they still seem to be moving in the right direction. But how are these scenarios designed?

Scenarios designed by studying extreme events of the past may not be accurate.

The scripts of movies and series are based on fictitious events. The publication of unreal events has become a popular literary topic! The scenarios built on the freight index are based on predicting the future.

If history has taught us one thing, it is that unusual events can result in significant changes. The Great Depression, the events of 9/11, the pandemic, although unknown and unpredictable, played an important role in shaping the global economy and politics. For instance, the 9/11 attacks prompted the FED to reduce interest rates, which inflated the housing bubble and leading to the 2008 financial crisis. The pandemic has led to the jump of the freight rate index, the return of the inflation monster, the inflating of interest rates, the deterioration of income fairness.

In other words, scenarios based on the surprise-extreme events of the past may not be true because each one is different. It's better to be ready for unexpected events than to use past data to set boundaries for the future. With this perspective, three very different scenarios were designed at the beginning of 2022 on the future of the freight rate index.

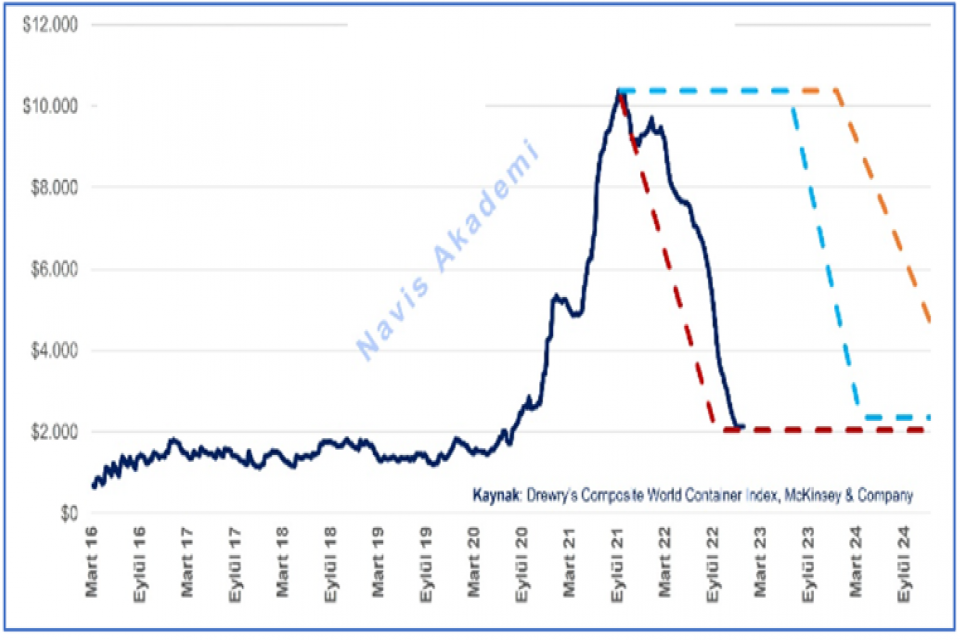

Diagram: Drewry World Container Freight Composite Index

Source: McKinsey

What do freight scenarios indicate?

If we remember the scenarios set up as we enter the year 2022, there were 3 different scenarios of assumptions about how the freight rate would proceed after the peak; Scenario-1 (Aggressive decline), Scenario-2 (Moderate decline), Scenario-3 (Continue to rise). It is clearly seen in the graph; When the year 2022 ended, the winner of the scenario race was "Scenario-1". If this scenario is undoubtedly consistent, it is highly likely that the freight rate index will continue its way with the saw movement as mentioned above. Of course, it would not be right to express a definite opinion. Let's see what kind of a freight rate index we will see at the end of 2023 at this time when the horizon line in the global economy is disappearing.

The information, comments and advice contained herein are not within the scope of investment consultancy.

Comments ( 0 )